Stone Soup, Diversification, and the Alchemy of Venture

One theme we talk about a lot in this newsletter is that startups aren’t economically sensible. That doesn’t mean they’re not valuable, or worth pursuing! But building the future is hard. Not only are you trying to build something that’s never been built before; you also have to finance it under really uncertain conditions. You can’t know what your own equity is worth, and you can’t really know how much you’ll have to raise. That’s not a great recipe for fundraising.

That’s part of why innovation ecosystems historically arise in clumps during specific opportunity windows, where capital is available more cheaply than it should be. This could happen for lots of reasons that we’ve talked about before: because the government has made it a priority, or because of a financial bubble or speculative mania, or as we talked about last week, when local angel investors are pursuing social status.

But even when you’re found one of those open windows, the “reasonable market rate” for your equity is still likely to be prohibitively bad, just due to the uncertainty of what you’re trying to do. You need to find someone who’s willing to buy your equity at better terms than you reasonably ought to deserve. Who might do this?

Here are two big reasons why someone could sensibly offer you cheaper-than-normal capital. Funny enough, they’re polar opposites of each other.

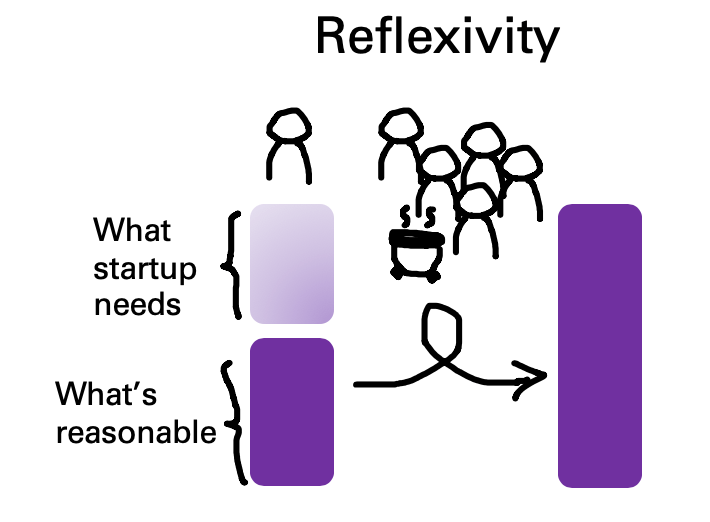

The first kind of investor is especially committed to seeing the business win. The person who does this most obviously is the founder. They’re committed to seeing their dream succeed, so they go all-in with their effort and probably their capital as well. Their dedication to the project makes them “overvalue” its prospects, but that overvaluing is important: in doing so, they reflexively unlock other resources, people and momentum on the way up.

Early employees and partners join in, as they agree to subsidize the business by taking smaller salaries so that the company stays alive. So do early investors who recognize that too-small valuations, even if rational, can kill companies before they start. If they’re going to commit anything, it has to be at generous terms, which hopefully become self-fulfilling. Auren Hoffman calls this the “Stone Soup Theory of Startups”: no one wants to eat a bowl of watery rocks, but when people become interested enough in the stew to contribute their own ingredients, you can end up with something delicious.

This early group of founders, employees, partners and investors, who become especially aligned and committed to the venture’s success, effectively make Stone Soup: they jump start businesses with a wave of reflexivity. When my unreasonable commitment (and “overvaluation”) of the business leads you to commit (and overvalue), and then the next person to commit (and overvalue), you can move mountains together and make that valuation come true. Reflexivity is a powerful thing, and as a founder, you’ll want it working for you.

The second kind of investor is the opposite: they’re not particularly committed to seeing the business win. When the startup is part of a portfolio, investors can offer you capital at more generous terms than if they were committed to you alone.

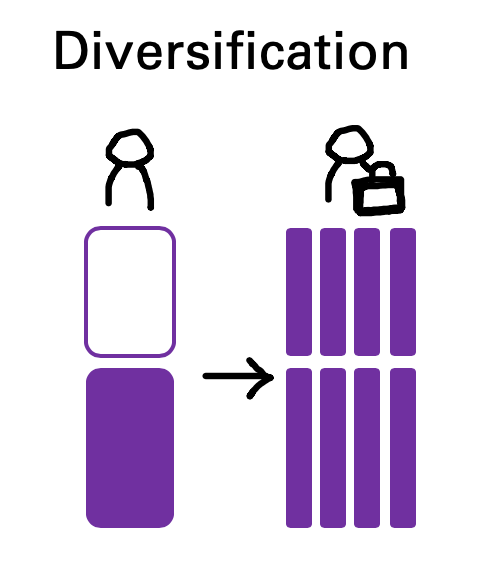

This may seem strange, but it’s how diversification works. If you own stock in only one company, you bear the risk and opportunity cost should that company fail. But if you own a basket of 100 companies, all of which are equally risky, you can get the same expected rate of return by owning the basket, yet face less opportunity cost – assuming the companies’ successes or failures are uncorrelated from one another and the cost of diversifying is cheap.

That’s why investors can rationally offer better valuations to a diverse basket of startups than than they could to a single concentrated investment. So it makes sense that investors can provide capital at cheaper-than-average cost if they don’t need this particular business to win.

This is a funny paradox! The people who can genuinely offer you the best valuations are either the people who care so, so much (because of reflexivity) or the people who don’t care that much (because of diversification). Weird!

Now if you had thought, “People that simultaneously care passionately about my startup, but also don’t really care that much because it’s part of a portfolio? Sure sounds like a VC!”, you’d be correct. Part of the dark art of VC is structuring your deals and your portfolio so that your fund, and by extension your portfolio companies, can take advantage of both of these phenomena at the same time.

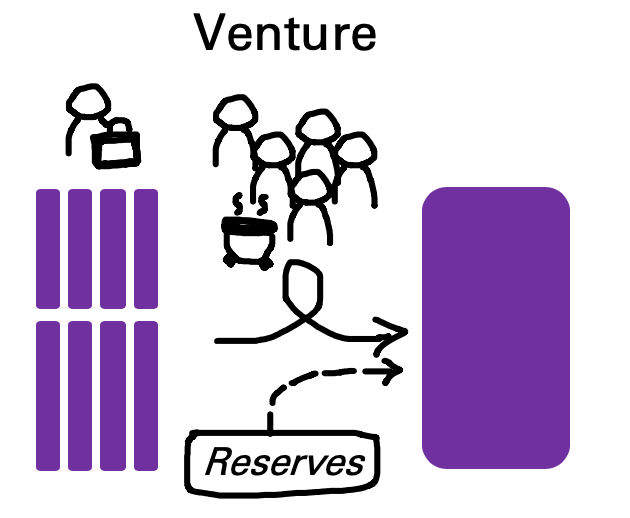

In order for a VC fund to work, you have to pull off two things simultaneously. First of all, your portfolio must be diversified enough to capture the upside of the current startup cohort without being overly exposed to the failure of any individual company, which happens a lot. A VC fund (and the LPs who invest in it) are willing to take on the risk of an entire crop of startups performing poorly, but not the risk of any one company. Diversifying helps bring the risk of a fund down to something more reasonable, so that VCs don’t have to demand prohibitively strict valuations.

But simultaneously, you have to fully commit to your investments, and you have to be concentrated in your winners. A venture round is not some day-to-day thing in the life of a startup; it’s a huge part of the startup’s ability to conjure its vision into reality. The more forcefully a VC fund can back a startup, the better are the startup’s chances. And down the road, if that business turns out to be Uber or WhatsApp, everything else you did in your fund will pale in importance compared to how much ownership you have in that one company. Percent ownership in your biggest winner is the number one factor that makes or breaks your fund’s performance.

A fund manager has to nail both of these simultaneously: the total concentration needed for reflexivity, but also the non-concentration needed for diversification. The VC model pulls this off in a clever way. VCs take what’s normally the biggest barrier in speculative finance – the inability to know in advance how much capital will actually be needed in future rounds – and use it to their advantage.

When a VC does a deal, they’re not just writing you a check; they’re also committing reserves in their portfolio to be invested in follow-on rounds, both to continue supporting the company and also to defend the VC’s ownership stake from dilution. These reserves cannot be literally committed, because we can’t really know when or how much they’ll be. But everyone involved understands that they’re there.

When done correctly, good reserve management by the VC lets them effectively have their cake and eat it too. The VC can get away with an initial investment that’s more generous than it normally should be (which can make a meaningful difference in the startup’s ability to recruit, execute, and make its Stone Soup), knowing that their reserves give them the option to concentrate later, allowing them to profit from being right.

But not every company will actually succeed and draw on their reserves, so VCs can effectively practice “fractional reserve investing”, and make a larger number of initial bets. In doing so, they unlock the magic free lunch of diversification: they gain the upside exposure, but with less opportunity cost. This also lets them offer initial investment terms that are more generous than they normally should be, which can be the difference maker for a cap table.

In the modern startup ecosystem, we take for granted that this works. But it’s a genuinely impressive piece of financial alchemy, and the innovation economy is the better for it. Ironically, once this technique matured into a higher “perpetual plateau” of startup valuations, the real benefit ultimately flowed to startups, rather than to the VC firms and their LPs. But that’s honestly okay by me!

It’s worth noting, by the way, that employees are also a significant buyer of company stock. But they cannot benefit from any of the financial magic that VCs lean on when they offer these generous valuations.

There’s no doubt that when a startup really succeeds, the employee option pool serves as a great tool for distributing some of that newly created wealth back to the people who helped build it. No argument there. And a couple decades ago, when option packages were novel and non-standard, negotiating for one could absolutely make a difference in your future wealth.

But nowadays, stock options and RSUs have become baked into compensation packages and expected salary levels in pretty much every tech company. And the outcome isn’t great for most employees. The deck is stacked against them, in both ends of the spectrum we’ve just talked about.

The first reason is that employees cannot diversify in the same way a VC fund can. It’s not for lack of trying – average employee tenure in the current crop of big tech companies is supposedly down to something like 2 years, compared to 5+ on average for older tech companies. But no matter how much they move, employees cannot build up a genuine portfolio of options that’s diversified enough for them to actually get the economic free lunch. If you’re not diversified, that valuation you just bought into is a fairly priced gamble, which usually isn’t a smart investment for regular people.

The second reason, ironically, is that employees cannot really concentrate either. Employees cannot manage their concentration of ownership in their employer the way a VC can. They have no “reserves”, and no equivalent of pro rata rights, to protect themselves against future dilution that inevitably comes with success and growth. For pure software startups, this might be fine, since rising valuations will outstrip capital raised if things are really working. But for all the bits-to-atoms startups that have to raise boats of capital to compete? Forget it: those common shares are only going to pay out in the rosiest of exit scenarios; otherwise you’ll get buried by the pref stack.

No matter how great it is to build the future, it is usually not economically sensible to invest into a startup (especially one you’re already working for!), because startups are not economically sensible things. Some investors – specifically, seasoned VCs with funds that are structured for these kinds of opportunities – are able to make the numbers work, and can get startups the high valuations they need. But that does not mean that those high valuations are a generically fair price. And it especially does not mean that buying in at that price is necessarily a smart thing for employees or non-sophisticated investors to do.

Like this post? Get it in your inbox every week with Two Truths and a Take, my weekly newsletter enjoyed by thousands.

Recent Comments