The Trillion Dollar Lawsuit

One year ago exactly, I wrote my first piece about a stablecoin called Tether.

A year later, uh, wow:

A complaint is not the same thing as a conviction. But the complaints are mind-blowing. This is not just “we are upset that we lost our crypto money and we’d like to sue someone”. If these accusations are found by a jury to be true, or even approximately true, then it will immediately go straight to the Hall of Fame level of Largest Frauds of All Time. In terms of monetary evaporation, the accusations here are ten times the size of WeWork, and at least ten times as interesting.

In my opinion, this is the most interesting story in tech this year and nothing else comes close.

The entire story is complex, and the lawsuit itself is admittedly over-the-top theatric (their trillion dollar damage estimate, for instance, is clearly for show rather than a sober legal petition.) But the accusations within it are real and serious. I’ve broken down the allegations into three parts:

Allegation #1: The 2017 Bitcoin Bubble was market manipulation, and Tether was how they did it

Allegation #2: Tether became a systemically important, money laundering conduit for the crypto ecosystem

Allegation #3: They might’ve gotten away with it, too, if they hadn’t gotten robbed while busy scamming

To be clear: everything I’m about to talk about here is an accusation, not established fact. It has not been proven in court. Many aspects of this story as I’m telling it may turn out to be misinterpreted or flat-out wrong. But it’s an important story, and I’m committed to sharing it with you accurately, to the best of my ability and understanding.

So, let’s begin.

Allegation #1: The 2017 Bitcoin Bubble was market manipulation, and Tether was how they did it

This is the part of the Tether story I wrote about most recently, back in June in All The Other Kids With The Pumped Up BTCs. Here’s a recap.

Unless you’re a crypto insider, the main lens through which you probably think about cryptocurrency and Bitcoin specifically is the price. The price of Bitcoin bounces around a lot, which makes sense: it is super speculative. Unlike something with intrinsic value, like a share of Apple stock or an actual apple, one Bitcoin is “worth” whatever the market feels it ought to be worth. And that feeling can change quickly.

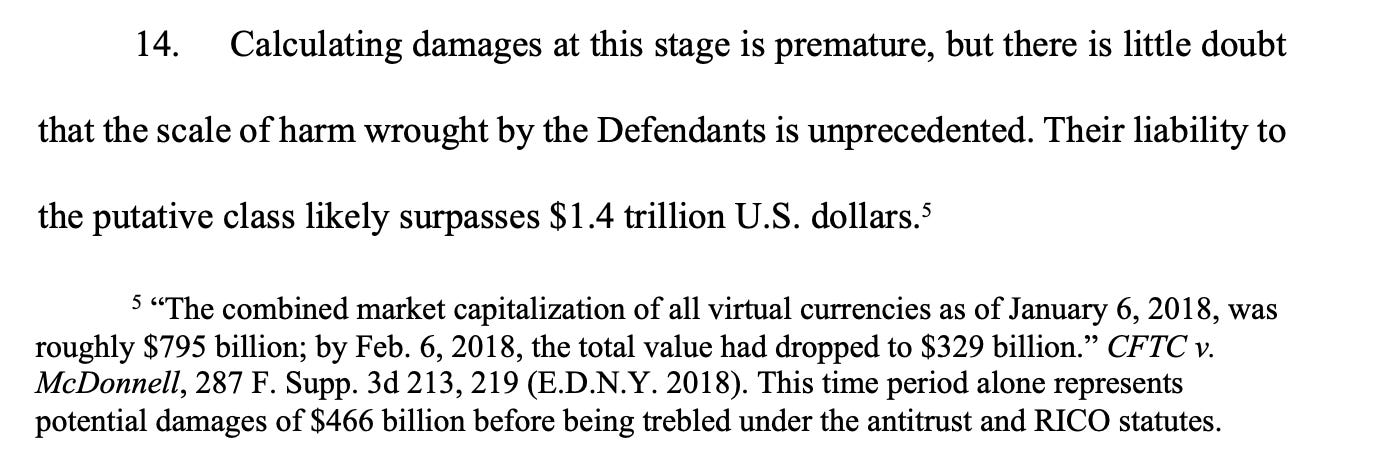

In 2017, the price of Bitcoin rocketed up from around $1000 all the way up to 5, then 10, 15 and close to $20,000 in less than a year, and then in the next year fell most of the way back down. If you include the other cryptocurrencies that rose and fell along with it, and measure from peak to trough, the total amount of speculative value that got created and then destroyed was over 450 billion dollars.

Why did this happen? The simple explanation is human nature: this was a bubble. No one knows what a Bitcoin is really worth, but if other people get greedy we get greedy too, and if they get afraid, we get afraid too. That’s why bubbles happen, like with the dot coms in 1999. Now, Occam’s Razor is usually right: sometimes the simple explanation is the correct one. But not this time.

We now know that what happened in 2017 was not just a bubble. It was also a scam.

To understand what happened here, you need to appreciate that the price of Bitcoin isn’t “real” like the price of Apple stock is – not only because it’s more subjective, but also for more serious reasons. Apple stock trades at high volume, every day, on stock exchanges that have rigorous, transparent rules in place to prevent market manipulation and abuse. Not Bitcoin. Bitcoin trades in the dark, on exchanges whose rules you don’t know.

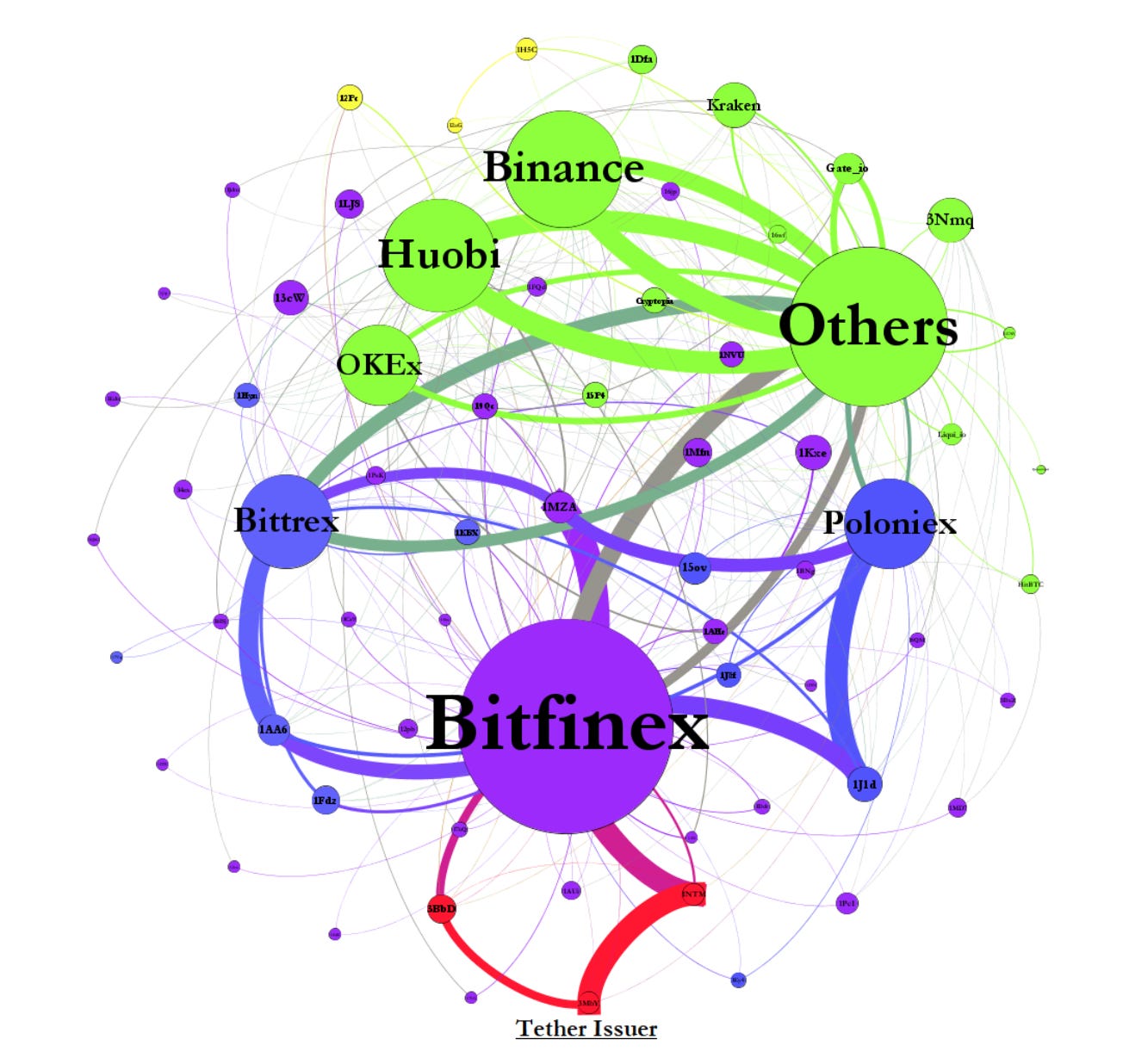

Bitfinex is one of those exchanges. At one point, it was the largest cryptocurrency exchange in the world. As you probably know by now, they worked with (and secretly owned) a Stablecoin called Tether that issued a cryptocurrency token pegged to a value of $1. Tether’s offering was essentially: approved customers could mail Tether a cheque for 100 US dollars, Tether would stick them in the bank for you, and then they’d issue you $100 worth of Tethers on a blockchain. You could go spend those Tethers on buying crypto, or doing whatever you want; when you’re done with them, send the Tethers back, and you get your 100 US Dollars back.

If Tether were acting honesty, and all Tethers in circulation were backed by genuinely invested dollars sitting in a genuine, safe bank account, then there’s nothing wrong with this. But that’s not what they did. Bitfinex and Tether, together with their business partners, figured out that they could use this money printing machine to their advantage. Here’s the basic playbook:

- Print a whole bunch of Tethers into existence – not backed by real dollars, but instead collateralized by other stuff – cryptocurrency, their own equity, IOU receivables, sometimes nothing. But most importantly, Bitcoin. Bitfinex held a lot of Bitcoin, which makes sense given they were the world’s largest Bitcoin exchange.

- Working with partners, flood those Tethers onto crypto exchanges all around the world (who treated Tethers as equivalent to dollars, sometimes indistinguishably so – more on this in part 2) to buy Bitcoin, pumping and stabilizing the price, and therefore pumping up the value of Bitfinex’s own Bitcoin holdings.

- If anybody asks questions (“Where did all those Tethers come from? Prove to me they’re collateralized”), sell some of your inflated Bitcoins for real US Dollars at a profit, stick those dollars in your bank account, and then say “Look! Here they are! Just like we promised.”

- Repeat.

Now here’s what I mean when I say that the price of Bitcoin isn’t “real”: when you see a Bitcoin price quoted on an exchange, you assume that the price reflects a bid/ask spread that’s genuine and deep. You assume that the bid and ask here represent actual investor interest, with real dollars – not an artifact of a thinly traded float, or from unbacked Tether dollars that were printed into thin air. Trading activity in the float makes it look like there’s demand to support the entire inflated “Market Cap” of Bitcoin and other cryptocurrencies, which is absolutely not true. But it looks true, temporarily.

However, because the price of Bitcoin is “whatever people want it to be”, and because humans are herd animals who get greedy when they see other people getting greedy, a surging price can bring in a new wave of retail investors, and turn the pump into a self-fulfilling prophecy. Even Bitcoin insiders, who may be more clued in to what’s going on, have no reason to be upset – they’re getting rich!

Once the price is successfully boosted, Tether is also useful for keeping things that way. If too many people try to cash out at once, Bitfinex can simply print more Tethers, buy Bitcoin with it, and keep the price up. Fortunately for them, many people who are actually investing into Bitcoin with real money are doing it because they believe it in over the long run. They’ll proudly carry their Bitcoin bags, and aren’t going to give up and sell on this week’s news.

Crypto markets can be too opaque and complex to accurately track as they move in real time. But for smart people who know what they’re looking at, you can create pretty good post-hoc reconstructions of what happened. After the bubble burst in early 2018, a lot of people were understandably upset that their paper gains had evaporated. So people started looking for what could be responsible, and that included the connection between Bitcoin and Tether.

John Griffin, a Texas researcher who is well known for uncovering fraud, published a landmark paper last year that asked the key question: was Tether used as a market manipulation tool in the Bitcoin bubble? They certainly thought so, concluding that Tether was overwhelmingly used as an instrument to “push” the crypto ecosystem, rather than being “pulled” by real market demand. ** Update: see footnotes

Is Bitcoin really Un-Tethered? | John M Griffin & Amin Shams

Did people know this at the time? Well, to varying degrees, yes and no. At the bottom of the crypto hierarchy, you have the typical bubble buyers: people who see their neighbours getting rich and want in too. They definitely didn’t know. Higher up, you have people who’ve spent time in the crypto ecosystem, have adopted some of the hubris and may have already gotten paper rich. They’re now way out over their skis in convincing their peers, and especially themselves, that their paper gains aren’t from luck, but actually because they’re a sophisticated smart person. They’ve probably heard of Tether, but not the whole story.

At the top, you have the real insiders, who are probably aware that crypto prices are routinely manipulated, and may even know some of the people doing it. But here’s the thing: none of these people want the music to stop. Even the insiders’ insiders, at the very top of the pyramid, probably genuinely believe that this market manipulation-y period is just a phase we’ll get through on our way to mainstream, legitimate acceptance of Bitcoin as the new gold standard.

Plus, even if you did know about all of this (as some people did, like @bitfinexed on Twitter, who I’m indebted to for helping us understand everything), it can be really lonely yelling “fraud” when everybody’s too busy getting rich. In a community built around a common dream of building a decentralized, prosperous future, worrying about all of this wealth being systemically exposed to a single, central point of failure won’t get you invited to many parties.

Speaking of single points of failure:

Allegation #2: Tether became a systemically important, money laundering conduit for the crypto ecosystem

But wait! You ask, perceptively. How does Tether get away with passing off their unbacked synthetic dollars as real, actual dollars? How did it become so embedded into the way the crypto exchanges operate? Good question!

Patrick McKenzie wrote a very good explainer of this aspect of the story a few days ago, which you can read here. I encourage you to take the time and read it through. I’ve summarized what I believe are the important points here.

In order for Bitcoins and other cryptocurrencies to have much value in the real world (and, especially, in order for people to speculate on them with real table stakes) you need some way to bring traditional currencies in and out of the system. You need real on-ramps to the world’s financial system; specifically, the US financial system.

If you run a crypto exchange, your customers are gonna want to buy, sell, and hold balances in traditional currency. To do that, you need a partnership with a bank. Annoyingly, banks have some degree of awareness that if they do business with criminals, they will get in trouble. So in order to work with you, banks require that you follow some rules, like KYC/AML compliance, which is fine in the real world but hard for anonymous online digital crypto exchanges.

Some of the more reputable exchanges do the hard work and make it happen; that’s why Coinbase asks to see your driver’s license. But many don’t. It goes against the culture: the whole point of cryptocurrency is decentralized, permissionless infrastructure for making transactions; enforcing KYC kinda kills the vibe there. Plus it’s also really hard.

Tether has stepped in as a kind of glue for all of these exchanges to quote, exchange, and hold US Dollar balances for their customers. As banks get more strict about partnering with crypto exchanges, Tether has replaced them, and in doing so, became systemically important to the crypto ecosystem.

I wrote about this exactly one year ago, in a long analogy about Pokemon cards. You can go back and read that piece if you want to. The important takeaway is that the customers using these unbanked crypto exchanges don’t know/care that the “Dollars” they’re trading back and forth aren’t really dollars, they’re Tethers.

You can understand the appeal here: Tether gave exchanges a way to have their cake and eat it too. If you’re only doing crypto-to-crypto trades, it’s easy to stay in the dark, but harder to deliver on the core promise of cryptocurrency for many of their users, which is “get me rich”. Tether gives you both, sort of – as long as it doesn’t break, and ideally, if you don’t cash out. Exchanges today freely quote US dollar rates and exchanges, but they don’t really use dollars. Without Tether, those exchanges freeze up.

As a general rule, you should be careful around investments that are easier to enter than exit. As exchanges lose their banking relationships, it gets harder to pull money out; as Tether replaces them, it remains easy to keep doing stuff with that money inside the ecosystem. Tether acts like a monkey trap for the whole system: once your hand is in the jar, Tether gives you this seductive freedom of movement to do whatever you’d like while inside. But it’s hard to leave.

To quickly recap here, we understand how Tether became systemically important to cryptocurrency exchanges by patching their banking problem. We also understand how Bitfinex and their partners took advantage of Tether’s ubiquity, and used the Tether printing press as a way to manipulate the price of Bitcoin and get rich.

Meanwhile – here’s where the story takes a turn in a new direction – Tether has actually found real product-market fit recently. It found a real, non-speculative use case among real customers with a job they needed done. Who might be interested in a conduit between people who have banking licenses and can interface with the real world, and people who don’t have banking licenses and therefore operate in the dark? Money launderers.

You know how people in crypto stubbornly insist that there is real crypto adoption out there in the world, for real financial purposes, just not where you’re looking? Well, they could be right! Millions of dollars (in Tethers) are supposedly crossing the China-Russia border every day, through a network of OTC brokers who use Tether to evade capital controls and fund who-knows-what activity. This is a bona fide use case for cryptocurrency, and for Tether specifically: swapping it back and forth, all day long, between people who maintain balances with each other across international borders, and who might not want report it.

And then there’s the bad stuff.

Meet the next key player in our story: Crypto Capital Corp.

Look, I know Tether and Bitfinex don’t look so great in this story so far. Sure, maybe they propped up the whole cryptocurrency market in the 2017 bubble, and tried to get rich off it. But, I mean, you can kind of understand their point of view: they care about crypto, they want the ecosystem to win, and yeah sure, they want to make a pile of money along the way. Who among us, etc.

They’re not the real bad guys. Crypto Capital Corp are the real bad guys.

Crypto Capital Corp is a shadow bank for criminals. Its president, Ivan Manuel Molina Lee, was arrested a few days ago and is accused of being a part of an international drug cartel and money laundering operation by Interpol and the DEA. Its principal mastermind, Reggie Fowler, was arrested earlier this year in the United States. We don’t know the extent of their business yet, but in order to get those kind of law enforcement agencies to work together, it’s usually because you did some pretty bad things.

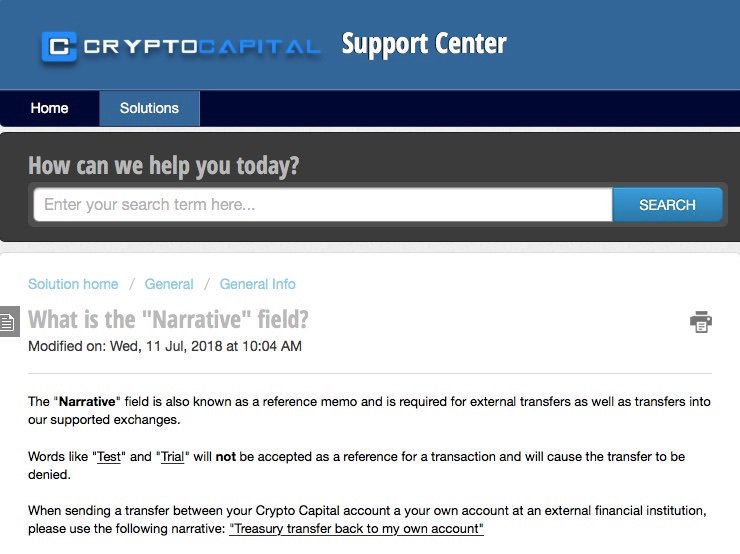

If you’re a criminal and you need access to the banking system, CCC does an important job for you. They set up shell companies and numbered accounts at sketchy, low-security banking establishments that don’t ask too many questions, advise you on how to send wire transfers in and out of that institution (helpfully suggesting narratives like “Treasury transfer back to my own account”), and then hold a balance for you in Shadow Bank Land, for you to go use for whatever hidden purposes you want.

I’m sure you’re not surprised to hear that Crypto Capital Corp inevitably became Tether’s bank. That’s when the story takes a turn for the truly ridiculous.

Allegation #3: They might’ve gotten away with it, too, if they hadn’t gotten robbed while busy scamming

Imagine you’re a scammer. You’re running a successful Ponzi scheme, and everything is going according to plan: your early clients have invested their money, you’ve shown them paper returns, and off of that gotten more investment capital, so you can start paying your early investors cash dividends. So far, everything’s on plan.

Then you discover something very bad. You check your bank account, and all the money is gone.

If you’re running a scheme of any kind, whether it’s a full-blown Ponzi operation or maybe it’s just a slightly off-books variant of a legitimate business, the cash in your bank account is your lifeblood for survival. Your cash is how you show legitimacy. It’s how you pay your bills on time. It’s how you keep the scam going. A scammer who gets robbed while they’re busy scamming is in big trouble.

The first two stories we talked about last week are both big but kinda vague accusations. “Market manipulation” and “Money laundering” can mean a whole range of things, and it’s possible we may end up with multiple versions of what happened accepted as truth by different groups.

The third story this week, on the other hand, is not. It’s fully literal, ties the whole story together, and is nearly stranger than fiction. It’s also a story as old as time: someone screws up, and they have to cover it up, and then they have to lie to cover up the cover up, and then they have to lie again to cover up the lie, building up a house of cards that you know will fall eventually. It’s just a matter of when.

So here’s what we think happened:

Bitfinex, who as you know was once the world’s largest cryptocurrency exchange (and also owns Tether), faced a classic cryptocurrency exchange problem a few years back. Nobody wanted to be their banking partner (see story #2, last week). Specifically, the Taiwanese institutions that Bitfinex banked with used Wells Fargo as their US Correspondent Bank, which is the on-ramp into the US financial system that matters. Wells Fargo, at some point, concluded that the relationship was too toxic and refused to give Bitfinex US banking anymore.

Bitfinex sued Wells Fargo over this, but it didn’t matter: they needed a new banking partner quick. After a brief foray with a Puerto Rican bank called Noble Bank, they settled on an institution called Deltec to hold customer deposits, and set up shop with our friends at Crypto Capital Corp to give Bitfinex the access to the mainstream financial system necessary to run an exchange.

On the surface, these were two separate banking relationships for two separate businesses. In reality, the relationship allegedly worked like this: In order to purchase Tethers, customers would wire $100 to a shell company under CCC’s control under some fake pretence; CCC would then credit Bitfinex’s account $100, and then Bitfinex would issue the customer $100 worth of Tethers. To get money back out, you’d run the process in reverse. In order to make this work, both Bitfinex and Tether held CCC accounts, and money would routinely get “swapped” from one account to the other, depending on which direction the process was running. In a sense, they used the combination of the CCC and Deltec accounts like a “hot wallet / cold wallet” setup, respectively.

Bitfinex and Tether routinely took advantage of this relationship; the division between the two was nonexistent in practice. (Remember this, it’ll be important later.) Apparently, this banking relationship was carried fully under the table: there was no written contract or legal basis at all for this relationship involving hundreds of millions of dollars’ worth of customer funds. But the relationship seemed to be working well.

However! Bitfinex’s execs failed to notice that while they were busy running Bitfinex and running Tether and keeping whatever it is they were doing alive, the good folks at Crypto Capital Corp were quietly embezzling their money. As US authorities noted when charging CCC’s principal architect Reggie Fowler with a variety of crimes:

Incredibly, it seems that Bitfinex failed to notice this was going on for some time. I mean, I guess it makes sense – if someone is laundering your money, you probably shouldn’t ask too many questions! That’s sort of the point! So long as you can get your money in and get your money out, the fact that it’s an un-auditable black box is a feature, not a bug. To CCC, you just need to make sure you can honour any withdrawal requests, and that 10% can go unnoticed for quite some time.

But then last year, something inconvenient happened: CCC got nailed by US authorities in a bid to uncover crime associated with Backpage, specifically money laundering and prostitution. One week later, CCC’s bank account got raided, as Polish authorities seized around $375 million worth of funds controlled by CCC companies. Fowler was arrested shortly afterwards.

This is obviously a problem for CCC, because the money they need to keep up their money laundering operation has been seized. It therefore created a bigger problem for Tether, because the money they need to keep their exchange and stablecoin running was seized / embezzled.

Did Bitfinex know that the money had been seized? It seems like no, they did not; at least not at first. But a few soon enough, Bitfinex started getting their withdrawal requests ignored or denied. This sure wasn’t ideal, as it accompanied a prolonged Bitcoin selloff that put pressure on Tether’s ability to maintain their peg (which, you’ll recall, was allegedly held up partially with Bitcoin and other cryptocurrencies, as opposed to real dollars). If you’re Bitfinex, you’re panicking over the next couple months. Where is the money??

You can read a pretty fabulous chat log exchange, which was presented as an exhibit in the Leibowitz court complaint, allegedly between someone at Bitfinex (Merlin in the log) and someone at CCC, addressed as Oz, on October 5 last year:

Merlin: Hey Oz, sorry to bother you every day, is there any way to move at least 100M to —–? We are seeing massive withdrawals and we are not able to face them anymore unless we can transfer some money out of Cryptocapital.

Merlin: I understand some of the funds are being held by —–, but what about the rest?

Merlin: under normal circumstances I wouldn’t bother you (I never did so far) but this is a quite special situation and I need your help, thanks

Merlin: I have been telling you since a while

Merlin: too many withdrawals waiting for a long time

Merlin: is there any way we can get money from you? Tether or any other form? Apart with cryptocapital we are running low in cash reserves

Merlin: please help

CCC: I know. We are following the banks we post as many as we can and let them process as much as possible according to them. Everytime we push them they push back with account closure without reason

Merlin: dozens of people are now waiting for a withdrawal out of cryptocapital

Merlin: I need to provide customers with precise answer at this point, can’t just kick the can a little more

Merlin: the international I mean

CCC: I will keep you posted here

CCC: On the process of all international payments.

Merlin: please understand all this could be extremely dangerous for everybody, the entire crypto community

Merlin: BTC could tank to below 1k if we don’t act quickly (Emphasis mine; see Story #1)

Meanwhile, incredibly, Bitfinex continued to send their customers through CCC, even while panicking about not being able to access their funds. Unsurprisingly, at some point they faced a liquidity crisis on the exchange. And so, we arrive at the real centrepiece of this whole story, a truly bonkers lawsuit from the New York State Attorney General’s office this past April. As spelled out in the lawsuit, Bitfinex truly went the extra mile in order to keep the exchange intact:

During November 2018, Tether transferred $625 million held in its account at Deltec to Bitfinex’s account at Deltec. Bitfinex, in turn, caused a total of $625 million to be transferred from Bitfinex’s account at Crypto Capital to Tether’s account at Crypto Capital, through a ledger entry at Crypto Capital crediting Tether’s account in the amount of $625 million and debiting Bitfinex’s account by a corresponding amount. The purpose of this exchange was to allow Bitfinex to address liquidity issues unrelated to tethers.

To spell this out if you didn’t catch it:

Bitfinex had a liquidity crisis on its exchange, because their money at CCC (the “hot wallet”) had been embezzled / frozen and they couldn’t meet outflow demand. Meanwhile, Tether has real money in their reserves account at Deltec (the “cold wallet”).

So Bitfinex does one of those swaps we talked about earlier, except at much bigger scale: they take $625 million of reserves backing Tether and transfer them to Bitfinex, and use it to plug their liquidity crisis. Then, they wrote an IOU against a matching $625 million in Bitfinex’s CCC account (which was frozen / stolen / didn’t exist) in order to credit their CCC account for Tether.

(Now is a good time to reiterate, by the way, that this is my best attempt at piecing together what happened. I could have elements of wrong. Anyway, read on.)

What Bitfinex is doing, in other words, is using Tether’s reserves as slush money in order to keep above water. Needless to say, they did not inform Tether holders that their deposits were no longer fully collateralized. Strangely, Bitfinex responded to this lawsuit by largely admitting that, yes, they actually did most of these things – but they did all of these things out of an abundance of caution protect their customers. (O..kay!)

So Bitfinex plugged their liquidity problem, but now they have a new problem, which is that $625 million worth of Tethers are now no longer backed by real dollars, but instead by IOUs for embezzled frozen dollars. Then, according to Bitfinex and Tether’s own lawyers (!!), the two entities “negotiated” a deal where the $625 million credit in CCC’s account was instead re-clarified as a loan from Bitfinex to Tether, now larger ($900 million) and that paid 6.5% interest. (Bitfinex had actually sort-of-successfully executed a similar tactic a few years earlier in order to make its customers whole after losing a bunch of Bitcoin in a hack, which is another story. There are so many stories! There is truly no bottom to this, people.)

By the way, there’s an interesting side question here which is: is it possible that Tether was actually fully collateralized prior to all of this mess? I mean, maybe? It still certainly looks like Bitfinex and their friends used their position in order to print Tethers as loans as opposed to deposits in order for their whale friends to pump the market, see Story #1. But if they had, then in fairness to them, they’d at least pulled it off. Until it stopped working, due to their money disappearing.

That’s why, as all of this came to light, Bitfinex backed up and dug into a position: “Yes, okay, we admit that Tethers aren’t fully fully collateralized with dollars. But they’re three quarters collateralized! That’s pretty good! Show me a bank with reserves that deep!” Of course, three quarters collateralized sounds a lot better than “backed by claims on seized assets, which we swear we’ll get back, we promise.”

Folks, repeat after me: if you’re going to run a scam (and please don’t do that, but if you must): don’t get robbed while doing it! Or, perhaps more specifically: try not to get into a situation where your bankers, who are robbing you while you’re out scamming, get busted by the feds! You’re gonna have a bad time! Oh and while we’re at it, you probably shouldn’t put down in writing something like “BTC could tank to below 1k if we don’t act quickly”, that won’t look good in front of a judge. That’s free advice.

So, now what? Well, Tether has a two-sided problem now. On the one hand, they need to somehow be able to honour their client requests, or else the stablecoin collapses. So it seems like they’ve resorted to a kitchen sink approach of throwing everything against the wall until it sticks, including now satisfying Tether withdrawal requests with cryptocurrency, Bitfinex’s assets (again, according to their own lawyers!), or anything they can get their hands on. Embarrassingly, seeing as they lost their main banking conduit in CCC, they’ve had to resort to asking “friends of Bitfinex” to help facilitate transactions, sometimes via their own personal bank accounts.

But on the other hand, they have to maintain kayfabe and keep up this absolute conviction that the IOU on the stolen money is still good! So they’ve had to make this public pivot towards arguing, “We are a legitimate business who was robbed by the criminals at CCC; once all of this gets sorted out, our money will be rightfully returned to us.” As more arrests get made and the curtain gets pulled back on what went down, it becomes an increasingly ridiculous charade. For instance, on October 25 – so, around two weeks ago – Bitfinex posted this official statement on their company website:

Several months ago, Ivan Manuel Molina Lee, a principal of Crypto Capital, was detained by authorities in Greece. This week he was extradited to Poland to answer charges there. Also, Oz Yosef (also known as Oz Joseph), another principal of Crypto Capital, has been indicted on three criminal counts by the U.S. Attorney for the Southern District of New York. As has already been mentioned publicly in court filings, Crypto Capital processed certain funds for and on behalf of Bitfinex for several years. During that period, Bitfinex relied upon various systematic representations from Crypto Capital, including from Molina and Yosef, that proved to be false. Among those misrepresentations, Crypto Capital regularly referred to its integrity, banking expertise, robust compliance programme and financial licences. This was designed to assure us that Crypto Capital was capable of handling Bitfinex’s transactions.

Bitfinex is the victim of a fraud (emphasis mine) and is making its position clear to the relevant authorities, including those in Poland and the United States. We cannot speak about Crypto Capital’s other clients, but any suggestion that Crypto Capital laundered drug proceeds or any other illicit funds at the behest of Bitfinex or its customers is categorically false. This week’s developments do nothing to affect or otherwise deter Bitfinex’s claims to funds in Poland or anywhere else. We will continue to work to recover all funds for and on behalf of our stakeholders.

I couldn’t help but emphasize “Bitfinex is the victim of a fraud” in their statement, because, look, they are the victim of a fraud! I honestly feel bad for them. Two years ago, they (allegedly) were doing illegal stuff all right, but if they had pulled it off, it could have ended up being one of those so-called “victimless crimes” where everybody in the ecosystem gets rich, they helped play a part, everyone loves them, and all of this gets swept under the rug of history. Instead, they got robbed by their own bankers, and then their bankers got arrested for being comic book villains who attracted too much attention to themselves by buying football teams.

So what did we learn here?

I can’t help but think of the incredible ending of Burn After Reading, where J.K Simmons is grasping at anything he can comprehend, and finally asks, in reference to John Malkovich’s character Osborne Cox: “Is he dead?” “No, sir, he’s in a coma.” Is Tether dead? …No, it’s not. It’s still there, like a weird half-conscious cryptocurrency protocol, like a grenade full of evidence with the pin pulled and the whole crypto community nervously staring at it, unsure of where to toss it or who to blame.

What did we learn here? I think my only honest answer as of right now is I’m not sure. I don’t know what this means for Bitcoin. I don’t know what this means for anyone with an investment thesis in any direction. I don’t even know what this means for Bitfinex and Tether, except for that I expect some people to go to jail.

But I do actually have one real lesson I hope you all learn from this. It has to do with the Monkey Trap analogy I touched on earlier.

The basic idea of a monkey trap is you have a narrow-necked jar with a bunch of treats in it: your hand can fit through it while it’s open and loose, but not while it’s clenched in a fist or while holding anything. Your hand is free to enter the jar. It’s also free to leave the jar, but only by letting go. If there’s nothing interesting in the jar, there’s no trap. But if the jar is really interesting, and especially if your hand is free to move, uninhibited, while inside the jar, it’s going to be really hard for you to quit.

The cryptocurrency ecosystem is like the jar. Inside the jar, people are legitimately building really interesting things, many of which are quite cool, and I look forward to seeing how it evolves in the future. But if you’re thinking about joining in, you need to understand the neck of the jar, which is the on- and off-ramps into traditional financial systems. Even if Tether were 100% legitimate, what it essentially does is supercharges our ability to do stuff inside the jar. But it does not make it any easier to enter or leave. (Unless, of course, you’re using Tether as a money laundering conduit to enter the jar through an illegal side door, like CCC.)

If the neck of the jar changes size for any reason – like, say, banks start to crack down on which cryptocurrency exchanges they’ll deal with – and it becomes harder to pull your hand out, it becomes all the more tempting to keep your hand inside the jar – you have total freedom inside! You can do anything! Look how much value we’ve created inside the jar! Look how amazing it is! This is true, but wait enough time, and you’ll learn the hard way how much the contents of the jar and the value inside the jar is really just levered on top of itself.

The crypto community may well learn the hard way that the only thing worse than systemic risk is systemic risk plus illiquidity. “Liquidity” inside the jar does not count. The only real liquidity that matters is through the neck.

I am nowhere near smart or qualified enough to predict what will happen from here on out. But if the people who’ve been paying attention are right, we’re in for a lot of pain when this band aid gets ripped off. And, unfortunately, it’s possible that a lot of people and projects who you’d never expect to be involved may get taken down with it: if you’re inside the jar, watch out. And just about everyone in crypto is in the jar.

**One footnote to mention: the Griffin study has since been updated after I wrote part 1 of this section in my newsletter. The updated study is even more bold with its claims, even suggesting that one single trader was responsible for the 2017 bubble. I’m not sure I buy this. I do more or less believe that a group of people successfully moved and manipulated the market, but that is not the same thing as what this paper claims. The updated Griffin paper, from what I can tell, mis-identifies pooled wallets used by exchanges as individual traders. To the best of my understanding, the pooled wallet-based conclusions in the updated Griffin paper neither support nor refute anything that was already presented in this debate.

**There are four people I’d like to thank specifically for what they’ve written:

Give them all a follow. You’ll learn lots.

Like this post? Get it in your inbox every week with Two Truths and a Take, my weekly newsletter enjoyed by thousands.

{kind=link}

Recent Comments