OuiWork? The quick case for WeWork as an actually disruptive business

So. WeWork, in whose co-working locations I’m sure many of you have spent time, is going public. It’s going for it at a time where – if you believe the news – the world economy is threatening to take a substantial dive. The business is valued like a tech company (in that it is hemorrhaging Softbank money for now) and the IPO prospectus is magnificently bold and vague about tech, mission, aggregation, community, and all sorts of scalable-sounding things.

But it’s quite unlike a tech company in that it’s selling something with distinctly non-software margins: office space. It’s also quite unlike a tech company in that it’s bringing along 33.9 billion dollars worth of lease commitments as it goes public. In its early years, WeWork enjoyed substantial discounts on these commitments (as is common in commercial real estate), but now they’re starting to come due in full and oh boy do they hurt. Can the unit economics work out in the long run? Can this business work?

So I set out this week with a goal of convincing myself that WeWork can plausibly win. And I think I almost got there? I’m not sure I believe they’ll win, but I do genuinely think that WeWork is disruptive – in the real sense of the word disruptive. Don’t believe me? Read on.

The We Company S-1 is like Tech’s version of the Mueller Report. It’s a Rorschach test that shows you whatever you were looking to see. If you previously believed that WeWork is a burning bag of dog turds, then you probably still think that, except now with numbers. If you previously believed that WeWork is actually a genius power move, then you probably still think that, except now with numbers.

There are so many S-1 breakdowns out there this week I’m not going to link to them all, save one: Byrne Hobart’s piece What is We!? Understanding the WeWork IPO. This piece is a good place to start, particularly since it dispels some of the hyperventilation around who-sold-what-to-whom that happens a lot whenever tech people read about a business in any other industry. For instance, yes, it’s actually quite reasonable for Adam Neumann to borrow money from WeWork, spend that money buying office buildings, and then lease those buildings back to WeWork. That’s basic separation of high-multiple and low-multiple assets; software people just freak out because they’ve never heard of the concept of a “low multiple asset”.

But anyway, back to our black and white questions. Is WeWork a bubble, or is WeWork an arbitrage? Is WeWork equity a real estate proposition, or a technology proposition? The WeWork S-1 repeatedly insists that it is a tech company, and ought to be valued like one. But where are its software margins going to materialize from?

Scale? I don’t buy it; not in the “we will achieve software margins at scale” sense. WeWork’s revenue comes from renting office space, and their cost of goods sold is… buying and/or renting that office space. That’s a perfectly fine business model, but it’s not revolutionary. Yes, there are services you can offer along with office space, but unless those services have software margins and can be effectively bundled into the WeWork office offering (a huge assumption) then we aren’t there. Network effects? Also no. There is zero advantage to joining the WeWork network because your customers, competitors, or friends are on it.

Aggregation? Come on. Commercial office space isn’t like buying diapers on Amazon or watching TV shows where the big variable cost is customer acquisition. Sure, WeWork may have a great brand and therefore be able to acquire tenants more cheaply than some random office manager. But that’s not the same as “WeWork is the choke point through which some critical mass of commercial real estate must pass.” I have seen some interesting ideas around how WeWork subscriptions might be an effective aggregator for other adjacent businesses like health insurance; that’s definitely a neat idea, but it’s not the core business.

The prospectus also helpfully includes several other key trends they indicate will drive “The Re-Invention of Work”: Urbanization, Globalization, Independent Workforces, “Flexible Solutions” (by which they basically mean, “shorter leases”), Workplace Culture, and “Sharing Economy”. (What? Who wrote this?) So, what, then?

I think a reasonable way to look at WeWork’s opportunity is as follows:

As software and the internet transform the workplace and eliminate friction from the commercial office space market, tenants increasingly resemble one another, and can be served in standardized ways. The more “atypical” a company’s needs (small, fast-growing, multi-region, seasonal, whatever), the more this matters: any customer can now be an easy customer. Shopping for square feet, whether it’s for a day or a decade and for one person or a thousand, is now all pulling out of the same bucket – just like Airbnb transformed short term residential real estate in a way where $200 / night and $2000 / month now have to compete with each other directly; as they should have all along, but never could before.

There’s an opportunity here to become a global scale low-cost, low-friction provider of office space. Professional office managers have always “used every part of the cow” in terms of carving up buildings and cash flows in order to optimally make everybody happy, but as friction and differentiation between one type of tenant and another type of tenant goes away, there’ll be an opportunity to create a low-end, good-enough, globally ubiquitous class of office space that can make money basically by squeezing as many tenants into as few square feet as possible while being able to juice occupancy by guaranteeing low rates for any duration of lease, for anybody, anywhere.

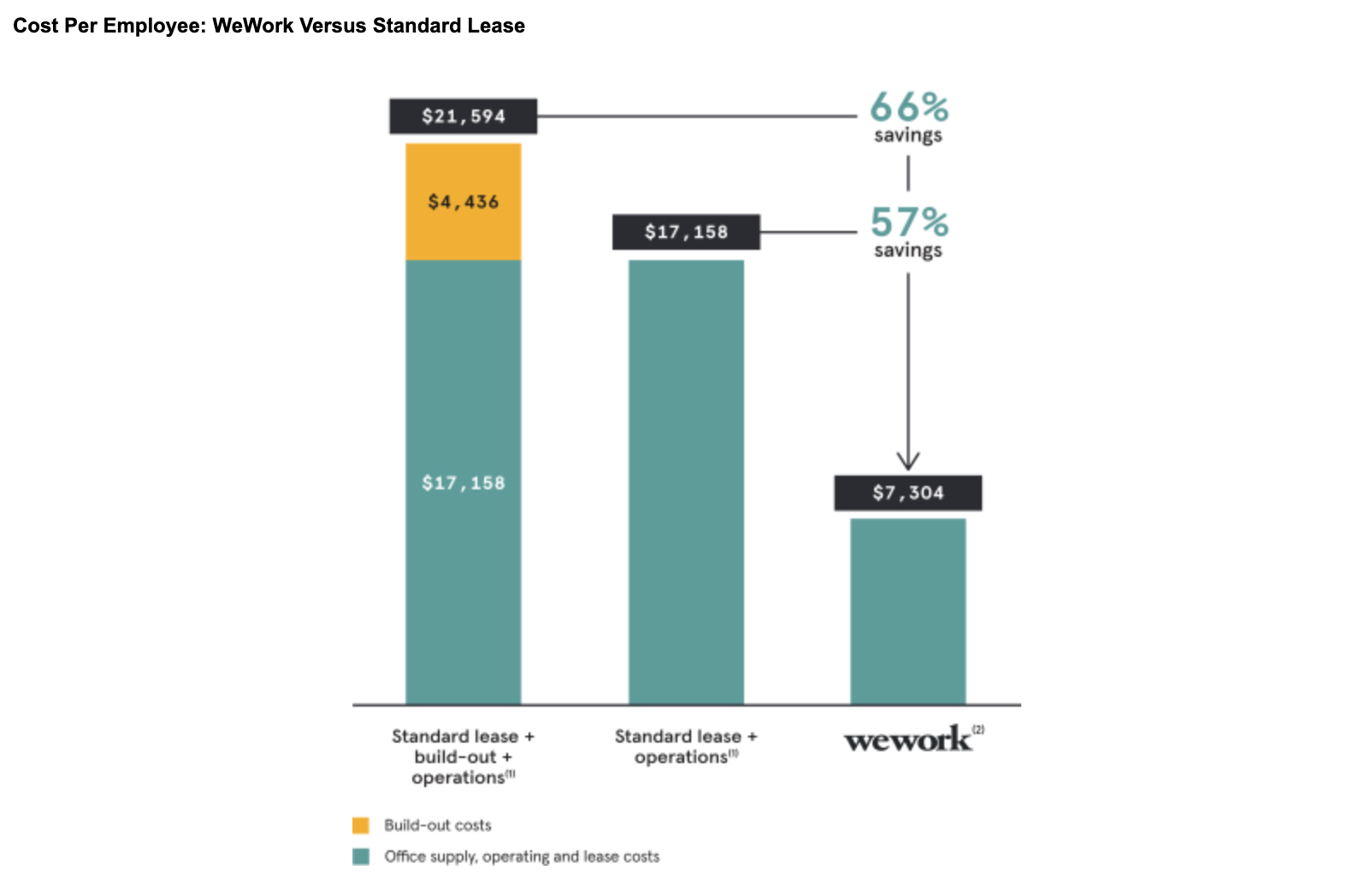

Despite the branding and the Instagrammable colour schemes and the beer on tap, WeWork is not a premium product. The fancy fruit water certainly helps reassure tenants that “you’re in a good place; you’ve made it; this is career success”. But don’t fall for it. WeWork is low-end on the main dimension that matters for commercial office space, which is what is the bare minimum of square feet that an employee needs, and what are the cheapest ways to distract employees from the fact that they’re working in an open-concept cattle pen? The lofty rhetoric around community and enlightenment are a key part of maintaining kayfabe. How are employees supposed to keep up the self-delusion if media coverage of WeWork is all about their tremendous cost-cutting efficiencies?

However, that doesn’t mean that WeWork is strictly a low-end product among all elements of performance that tenants care about. WeWork’s competitive advantage is that it’s lower-friction than anybody else. It’s fast, it’s standardized, it works for you, you can get an affordable office space today if you need. They do genuinely live up to their branding as a “tech company” along this element of performance. Software and the internet don’t make WeWork space any cheaper or nicer, but they do make it available faster, with less friction, than any incumbent can match.

WeWork is genuinely “disruptive” – in the original Innovator’s Dilemma sense. They are a low-end disruptor, providing an inferior but good-enough product to cost-sensitive customers who are overserved by traditional corporate office space, but underserved along a new element of performance (speed, flexibility, standardization, “space-as-a-service”, whatever you want to call it.) If you’re an incumbent who makes money by selling square feet, that’s not attractive for you to compete with. The better move for incumbents is to retreat upmarket, and not poison their income statement by renting discounted desks one by one to freelancers.

Now, here’s where it gets fun: how will WeWork keep up an economic moat in this new world, and sustain an attractive multiple on earnings (once it has them?) If it’s a race to the bottom, what’ll stop other people (particularly incumbents) with cash, experience, and other advantages from simply diving in after them?

Well… would you want to compete with them?

I have a thought here that I can almost say with a straight face. If WeWork can raise a giant pile of cash in its IPO and then not die in a multi-year recession starting any time now, it could find itself in a position where no one else is able to raise and money and get off the ground to compete with them without dying first. All the while it’ll be able to scoop up even more cheap commitments while times are lean, back-loaded in the usual way. That could actually turn into a real economic moat, like the classic example of trying to fund a second storage locker business in a town that already has an existing, massive storage locker facility. There’s just no point.

That back-loading typical of commercial office space contracts may turn out to be important. If they can get really fast at spinning up offices and filling them with tenants who all pay full freight (cheap as it might be, relatively speaking) then that’s positive cash flow. WeWork gets cash in the door before they start having to pay it back as cost of goods sold to their own landlords. It’s really scary to compete with a business that is operating at revenue break-even but cash flow positive, if you’re starting from behind.

I suspect WeWork is banking on this being a key aspect of their economic moat. If they can get really fast at spinning up offices and get to enjoy a few years of actual, bona fide positive cash flow from each before their COGS comes due, and assuming that speed of spinning up offices for these kinds of businesses is proportional to how big you are (reasonable, I think) then it becomes formidably difficult for anyone else to break into this low-end, good-enough market before too long. (The assumption here, by the way, is that new entrants will not be able to play comparable cash flow games because they don’t have the deployment experience, scale, or order book to actually extract those few years of cash. Their revenues will only materialize as their costs do, too.)

Note, by the way, that this is crucially different from businesses like Uber and Lyft, who also face criticism for not being differentiated or having an economic moat in any given location. The difference has to do with switching cost for customers. When Lyft enters a city where Uber is already operating, you can start poaching riders and drivers on day one, since there’s effectively zero switching costs for either. But with office space, there’s substantial switching cost. If you want to poach tenants away from WeWork, it’s going to take time as their leases run out and they move spaces; during which you’re losing that key window in which you can generate the positive cash flow that makes the whole thing work.

This is the most un-software like moat possible: “You can’t compete with us because you’ll die first.” Their S-1 might be conjuring up this incredible fiction of software buzzwords, but… I mean, so what? Is the goal for them to conjure up some impossible software-margin pipe dream, or is the goal for them to win?

It takes a whole lot of stones to say, with a straight face, that you’re raising money for a business that’s going to command 30x multiples for a bunch of fancy sophisticated tech reasons, and then use that money to build a wall out of one dollar bills. But… but… what if it works! Just think about the case studies there’ll be; about how everyone missed this because we read the WeWork S-1 expecting it to show, “no one can compete with us because we’re so great”, but then it actually turned out to mean, “no one can compete with us because we’re so terrible.” That’s real disruption!

This might be one of the most pure, uncut disruption theses I’ve ever seen, the more I think about it. It’s especially sweet given how Silicon Valley has somehow convinced itself that “disruption comes from the high end now”, or whatever people said to twist the Innovator’s Dilemma into knots just so they could say that Tesla and Uber were disruptive. I’m already enjoying how fun it’ll be to remind people: “and the real disruptor was… WeWork, all along.”

Does it mean it’ll work? lol no. Genuine disruption usually doesn’t work out, especially without some major technological force that differentiates the underdog, rather than pure low-end disruption economics. The majority of smart people reading through this S-1 have concluded that WeWork will blow up as soon as things turn south, and I mean, they’re probably right. But it’ll be super fun to see if the disruption thesis turns out to be right. I’m certainly watching with interest.

There’s only one real take-home message from this, by the way. If you look at a business and your takeaway is “this business is terrible!”, before you write it off completely, ask: “could this be disruption?” It just might be.